Chanel is taking a hard stance when it comes to sales of certain handbags and leather goods, with the French fashion house making headlines this week for putting a strict limit on the number of bags that consumers in certain markets can buy over a one-year period. The Korea Times reported that on the heels of raising prices in February, July and September of this year, Chanel has adopted a new policy in Korea in which “each customer can buy one Timeless Classic flap bag and one Coco Handle bag per year,” and has also put quotas in place for on small leather goods, including wallets and pouches, assuming that “a customer wants more than one of the same model in the category.”

Not the only brand placing limitations on the sale of certain products, Chanel is joined by Hermès, which has notoriously limited the quantities that consumers can purchase of certain “quota” bags, namely, Birkin and Kelly bags, to two bags per a calendar year in furtherance of a “very limited distribution strategy.” At the same time, the Korea Times reported in September that Rolex has similarly been “restricting per-capita purchases,” in the Korean market, at least, in light of raging demand and limited supply. Dating back further, Louis Vuitton has been known to limit consumers’ abilities to purchase more than two of each handbag style per calendar year in an attempt to put a halt to “professional buyers” who were purchasing and then reselling luxury goods “through small shops throughout Asia, or through online retailers like eBay,” the New York Times reported back in 2008.

The aim for Chanel is largely the same: it is working overtime to ensure that its hard-earned luxury positioning remains intact and not at the mercy of the burgeoning resale market, where it has no control over the products being offered up, the condition of those goods, and the manner in which they are marketed and sold. The brand has reportedly doubled-down on that effort by replacing the authenticity card-and-serial number combination that was traditionally used to authenticate its bags with microchips that can only be verified/authenticated using Chanel technology. (This falls neatly in line with the assertion that Chanel made in the lawsuit that it filed against The RealReal that the “only way for consumers to ensure that they are in fact receiving genuine CHANEL products is to purchase such goods from Chanel or from an authorized retailer of Chanel.”)

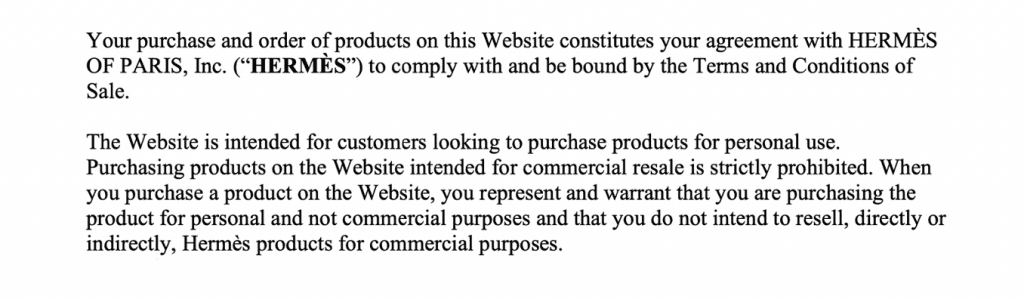

Hermès has taken things a step further, adding language to its sales receipts in an apparent attempt to block buyers from reselling their purchases in certain capacities. As Pursebop revealed late last year, the Paris-based luxury goods brand began adding language to its receipts in or around July 2020 that states that as a term of sale, “The customer represents and warrants that they are purchasing Hermès product in our boutiques for their personal use. Therefore, you agree you will not, directly or indirectly, resell Hermès products purchased in our boutiques for commercial purposes.” TFL has since discovered that the terms of sale for hermes.com also include similar language.

How Chanel, Others Approach Resale

Product quotas and the addition of elements, such as specific commercial resale-prohibiting language on purchase receipts, is an indication of how some brands are dealing with the resale market. At the same time, it is a demonstration of how brands’ strategies can vary quite significantly when it comes to the swiftly-growing resale market.

The likes of Chanel and co. are among those looking to get a handle on the secondary market and have been for years. Chanel, for instance, filed suit against reseller Fashionphile back in 2014, a precursor to additional resale battles that it has since waged against The RealReal, What Goes Around Comes Around (“WGACA”), and Crepslocker, among others. (WGACA has argued that the only resale that Chanel will tolerate is Farfetch due to its equity stake in the retail platform.) All the while, Chanel has been openly fighting unauthorized gray market sales for years, with Bruno Pavlovsky, Chanel’s president of fashion, stating back in 2016 that the brand had “reduced quite a lot the parallel market, mainly in Asia.”

This approach makes sense in that no shortage of luxury goods brands have been hesitant to embrace resale by fear that it will negatively impact their sales of new products, and at the same time, will chip away at the carefully-crafted image of exclusivity upon which they depend. (Logistics also present an issue, but arguably not one that groups with the scale of Chanel or LVMH, for example, cannot take on.)

Not all brands are taking such an openly tough stance against resale. A number of Kering-owned brands, for example, have entered into resale partnerships with established resale players. Gucci teamed up with San Francisco-based resale giant The RealReal last year for a limited partnership, and more recently, began offering up pre-owned products by way of its new Vault Venture, while Alexander McQueen revealed a partnership with Kering-based secondhand luxury marketplace Vestiaire Collective early this year. It is the view of Kering chairman and CEO François-Henri Pinault that “rather than ignoring” resale, which he describes as “a real and deeply rooted trend especially among younger customers,” Kering is angling “to seize this opportunity to enhance the value we offer our customers and influence the future of our industry toward more innovative and more sustainable practices.”

(It is worth noting that there are successful examples of the secondary market being owned at the upper end of the spectrum in the auto space. “Selling pre-owned luxury cars is a prominent element of the revenue model of luxury automobile dealers,” according to HEC professor Jean-Noël Kapferer. “The first clients registered on waiting lists for the newest Ferrari model often already own one and expect to sell it back to their local dealer.” The pattern of automakers and/or their authorized dealers buying back used cars and selling new ones has “various benefits,” per Kapferer, in that “it establishes a seamless, continuous client relationship; helps control sales regionally; and makes the brand available to new clients who might not have the budget to afford the latest model or who do not want to suffer the typical 20 percent drop in value in their first year of ownership.”)

Benefits to Buying In

Chances are and assuming that luxury resale – which was worth a reported $24 billion in 2020 – continues to grow (and it is expected to), brands that are the most hesitant to embrace resale will have to, and will likely aim to own the market for their pre-owned products by bringing resale efforts in house or linking with an established resale player to be able to enjoy greater control over the market.

With such demand in mind, sitting out on resale – either by not partnering with established retail entities or by failing to roll out their own in-house ventures – brands are missing an opportunity to reach (and bank on) the growing pool of consumers that are actively buying pre-owned luxury goods, albeit from unaffiliated outlets.

A potentially bigger driver, though, stems from the fact that the appeal of the resale market is so intrinsically linked to the original brands at play (and their trademarks). Even if there is not an affiliation between a resale entity and the original brand (and there often is not), there may as well be. This is because a significant part of what the consumer is buying into when it comes to luxury goods (either in an initial sale or a resale capacity) is the brand, itself. As such, when a resale company markets and sells a Chanel-branded bag, for instance, the appeal, reputation, goodwill, etc. of Chanel is the biggest draw, along with an attractive price tag, of course. (This affiliation-centric argument is at the heart of the lawsuit that Chanel filed against WGACA back in 2018).

It follows from this that if there are issues with the authenticity and/or quality of a product sold in a resale capacity, it will not merely reflect poorly on the resale company, there is a chance that such consumer dissatisfaction will be imputed back to Chanel – even if the brand had nothing to do with the sale, thereby, posing a risk for companies whose entire ability to sell products at a marked premium depends on their reputation among the consuming public, something that they have spent hundreds of millions of dollars (or more) building up over decades.

With that in mind, and given the built-in competitive advantages that luxury brands have over third-party resale entities thanks to their ability to gain access to inventory and to authenticate products with certainty, luxury brands should be eager to become involved, if for no other reason than a quality control perspective.

Share