Deep Dives

Non-fungible tokens – or “NFTs” – are rapidly garnering headlines, as the unique blockchain-based tokens take a wide range of forms – from artist Beeple’s 5000 Days’ NFT collection (picked above), which sold for $69.346 million in a Christie’s auction last week, to Dapper Labs’ NBA “Top Shot” product, a blockchain-based trading card system that has generated over $230 million in gross sales since October 2020. A buzzy new form of blockchain technology, NFTs “can represent almost anything,” according to Pillsbury lawyers Carolyn S. Toto and Chaz Hales, who note that NFTs have been “growing significantly in popularity in recent years because of their potential to ‘tokenize’ anything and provide a way to transfer ownership of digital assets to holders,” operating quite a bit like traditional “a certificate of authenticity.”

The NBX x Dapper Labs’ collectible digital assets – “trading cards” that swap out a traditional photo for a short video clip of a “top” moment from a key player – provide a look at how the technology works. “NBA Top Shot is a crypto-collectible consumers can purchase as an NFT,” CNBC reported late last month. “Each collectible is tied to a blockchain – a digital ledger similar to the blockchains used for digital currencies like bitcoin.” This “effectively gives each NFT a unique and non-hackable certificate of authenticity,” which makes it so that “even if somebody makes a perfect copy of the highlight video, it will instantly be recognizable as a fake.”

To date, the notion of NFTs has existed almost entirely in the digital realm – with eager buyers snapping up digital animations created by musician Grimes, RTFKT’s online-only sneaker designs, Top Shot trading “cards,” etc. In terms of what people are actually buying, that is the unique token and the work of digital art linked to that token. When as sale occurs, the transaction is registered on the blockchain, which means that it comes with a permanent and transparent record of that purchase and a buyer’s proof of ownership.

With the new NFT-linked assets in their possession, buyers can then display these digital goods (albeit in something of a different sense than a tangible painting or sneaker, for instance), or they could resell them, a documented process that requires a blockchain transaction that can be authorized only by the NFT owner’s private key (much like sending Bitcoin or any other cryptocurrency), further continuing to ensure authenticity and appropriate ownership.

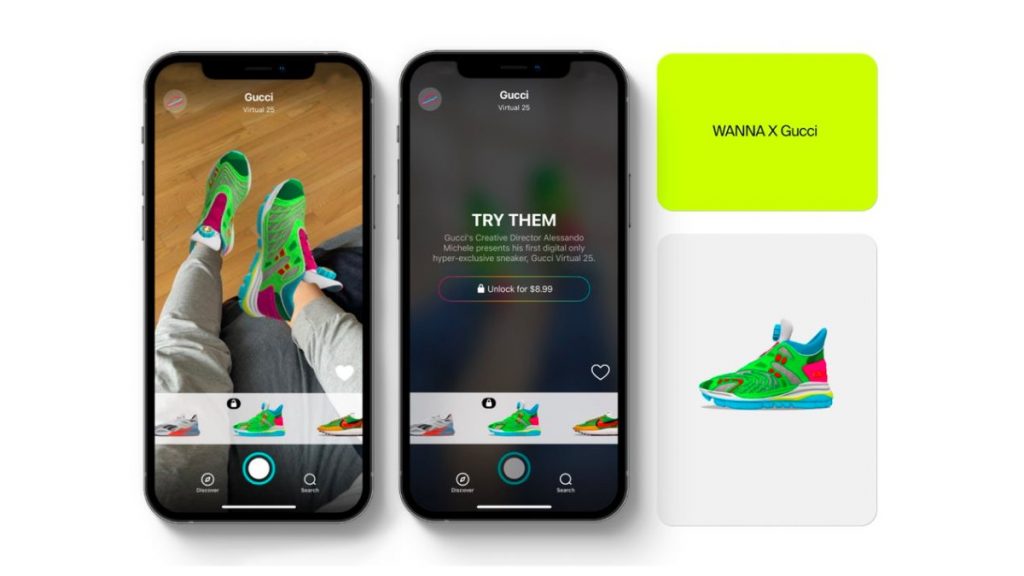

If Gucci is any indication, luxury brands will almost certainly venture into the world of digital assets. This week, the Italian fashion brand released its own virtual sneakers with Bularus-based fashion-tech company Wanna. The new footwear – which ranges in price from $9 to $12 – “will be available for purchase exclusively on Gucci’s mobile app,” per W Magazine, enabling “users can flex them on a variety of other digital spaces and game avatars, including Roblox.” (Note: Gucci’s sneakers are an example of virtual fashion offerings generally, and are not linked to NFTs.)

The more interesting issue, however, is not whether luxury brands will rush to embrace virtual fashion and corresponding NFTs, but whether NFTs – which are not the assets, themselves, but electronic records representing ownership of assets – can be linked to physical products to bring the same authentication and traceability benefits that exist for Beeple’s nearly $70 million artworks and the tokenized version of Twitter founder Jack Dorsey’s first-ever tweet (currently, the highest bid for the March 2006 tweet, which reads, “just setting up my twttr,” is $2.5 million) to the physical realm. Experts say that the answer to that question is yes: NFT technology can, at least in theory, be extended to anything, physical assets, included.

The concept – or more specifically, the authenticity-specific and transparent recordation aspects of such scenarios – is certainly compelling, and while inherently cyber-in-nature, the facets of NFTs have implications for and have sparked interest among luxury goods brands, which are consistently facing issues over the widespread sale of counterfeit or otherwise infringing goods, something that has arguably been amplified in light of the rise of the resale market.

Using NFTs for proof-of-authenticity purposes is not unheard of. In fact, early NFT-adopter Arianee announced last week that it raised $9.6 million from French investment bank Bpifrance and France’s leading seed investment company ISAI to further develop its luxury-focused blockchain, which takes the form of “NFT digital passports for luxury goods” in order to “guarantee the authenticity [of the linked products], and secure resale,” fintech site DailyCoin reported this week.

As it turns out, CoinDesk’s Ian Allison echoed, “Blockchain-based watermarks – or digital passports – to verify the authenticity of luxury items like high-value watches are a solid use for Arianee’s technology, often using the concept of NFTs that are currently very much in vogue.”

Founded in 2018 Pierre-Nicolas Hurstel and Frédéric Montagnon, Arianee and its use of NFTs “is reinventing the customer relationship with fashion and luxury goods players through a unique value proposition based on the digital identity of an item,” Bpifrance’s Guillaume Simonaire said in a statement this week, referring to the company’s provenance-tracking technology, which not only aims to verify authenticity and establish ownership of luxury goods by way of an NFT-centric watermarking system, but also goes so far as to digitize service history and repairs, a critical consideration for the likes of luxury timepieces (as we know from Rolex), and handbags, judging by arguments made in the Chanel v. What Goes Around Comes Around case.

(Unsurprisingly, Arianee recently partnered with watchmaker Breitling to ensure that all new Breitling watches are offered with “a fixed digital identity that is unique to each product, using blockchain technology to ensure airtight security and privacy.” At the same time, CoinDesk notes that Paris-based company’s “technology is also being used by Switzerland-based luxury goods conglomerate Richemont Group.”)

“Proof of authenticity is a compelling use case for blockchain that stands apart from most enterprise uses of the tech,” Allison says. As a result, it is not shocking that Arianee – which says that its tech “unlocks a new paradigm of digital value on top of each item” – is not alone when it comes to provenance-tracking.

LVMH, for example, revealed in March 2019 that it had been working on a blockchain-based system called AURA alongside Ethereum design studio ConsenSys and Microsoft, which is aimed at authenticating luxury goods by enabling consumers to trace the origins of their products given that “every step of an item’s life cycle is registered, enabling a new and transparent storytelling.” (LVMH also asserted that the tech could be used to “protect creative intellectual property and counter advertising fraud”).

With the exception of news that LVMH-owned watch brand Hublot will implement an electronic passport and warranty system for all its watches in order to fight fakes and simply the warranty process (with such e-warranties registered on the AURA network), little has been made of LVMH’s grand reveal almost two years ago.

Looking at the striking rise of NFTs generally, Frankfurt Kurnit Klein & Selz PC attorney Jeremy Goldman says that “as the once-obscure technology gains mass appeal and rapidly evolves into a mainstay of popular culture, companies and individuals across the globe are racing to jump aboard the NFT train, exploring whether and how they can leverage NFTs to connect with consumers, extract new value from existing and newly created digital assets, and generate new streams of income.”

With the widespread rise in adoption, of course, comes many other issues that brands will need to consider, according to Goldman – from how they can “clearly and conspicuously ‘attach’ terms and conditions to an NFT and ensure that those terms follow the NFT and bind subsequent owners,” and how “NFT platforms, issuers and intellectual property rights holders can limit their liability” to how the First Sale Doctrine operates in the world of NFTs. Many of these questions will likely be answered as NFTs continue to gain steam.

In the meantime, artist Krista Kim recently debuted the world’s first NFT house, complete with “a calming musical accompaniment” courtesy of a partnership with Smashing Pumpkins musician Jeff Schroeder. Called the “Mars House,” it sold for $512,712 after being “on the market” for 2 days. The COVID housing market is hot.