“All luxury categories underperformed” in China in 2024, “with beauty doing better and watches and jewelry performing worse,” Bain & Co. asserted in its latest luxury report, which looks exclusively at the Chinese market. The market consultancy found that “only a very small number of brands enjoyed growth in China in 2024,” noting that the success of these companies “is not driven by scale, as we see small and large brands among the winners.” Part of the problem has stemmed from the pricing disparities between luxury goods in China and other markets, particularly Japan, which prompted a resurgence of overseas luxury shopping in 2024 to the detriment of sales on the Chinese mainland.

> Historically, in response to striking price differences, some brands have “implemented a global pricing strategy to offset most of the exchange rate fluctuations,” per Bain. However, this year, brands opted to address these price disparities by “implementing purchase limits in stores and aligning new product prices globally (in the fourth quarter).” Ensuring “more controlled global price difference and swift reactivity should be a top priority for luxury leadership teams in this turbulent macro environment,” Bain states.

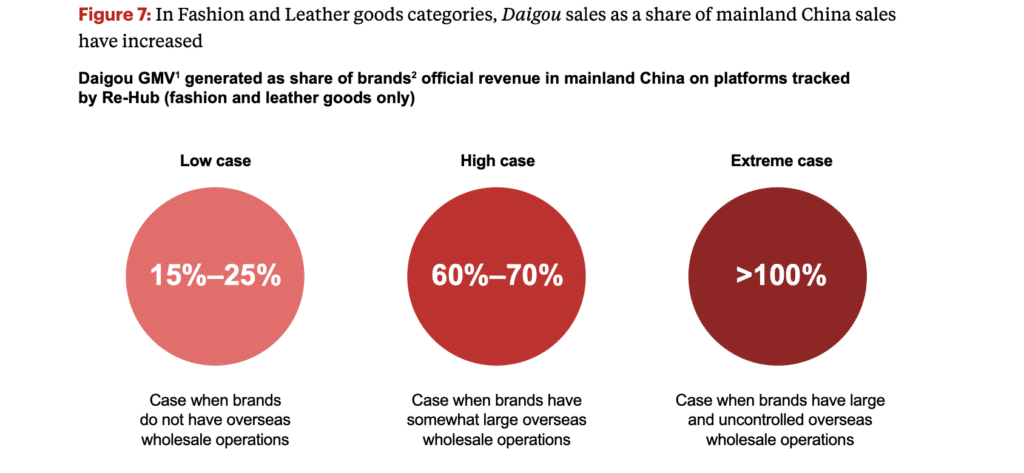

While there may have been a decline in sales of luxury goods via companies’ authorized distribution chains in China, increases came by way of off-channel sales – or sales of grey market goods. Demand for “genuine branded goods obtained from one market (i.e., a country or economic area) that are subsequently imported into another market and sold there without the consent of the owner of the trademark” – which are better known as daigou in China – was particularly prominent in the fashion and leather goods categories, Bain reported. In fact, Bain puts growth of the overall grey market at 5 percent for 2024.

“Favorable exchange rates, pricing discounts, promotion mechanisms, and so on have reignited the potential for small-scale daigou operations to blossom,” but Bain explained that “the main source of supply [of grey market goods] is likely from large-scale or professional daigou, which benefit from substantial pricing advantages through wholesale distribution channels.”

Discounts for the top products – including coveted bags, footwear, and jewelry, among other goods from the likes of Louis Vuitton, Chanel, Prada, Gucci, and Hermès – on Daigou platforms “deepened by approximately eight percentage points in 2024,” according to Bain, which cautioned that “this trend raises concerns that the grey market will continue to undermine revenue potential and brand equity on the Chinese mainland.”

To counteract this trend, Bain encouraged brands to “prioritize addressing daigou operations strategically in 2025 and beyond, [which] can be achieved by optimizing wholesale operations worldwide; harmonizing price gaps” – something that companies have largely opted not to do – and “focusing on enhancing customer relationship management, aftersales services, and overall client experience on the Chinese mainland.”

The bottom line on daigou: “Brands should prioritize enhancing brand desirability and delivering genuine value through initiatives such as brand-building events, creativity, product innovation, and improved client experiences to retain consumers domestically and capture market share from competitors. Additionally, China should not operate in isolation; it should seek global collaboration on pricing and daigou sourcing, especially on global wholesale operations.”

This is a short excerpt from a weekly briefing that is published exclusively for TFL Pro+ subscribers. For access to all of TFL’s content, including our weekly briefings, inquire today about how to sign up for a Professional subscription.

Share